Latest Chemical Industry

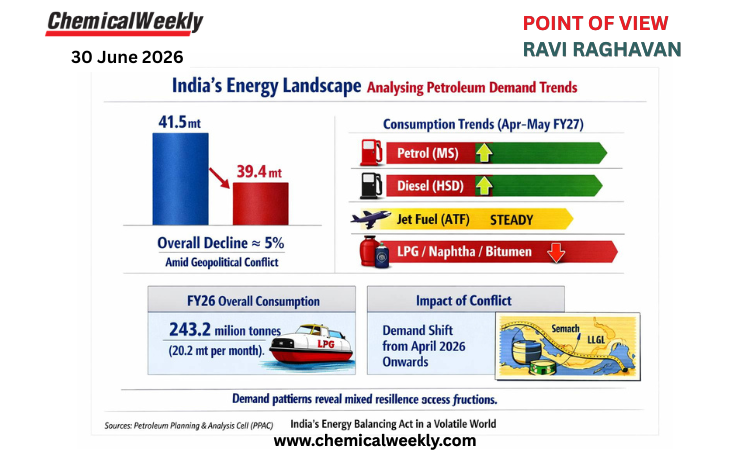

India’s energy landscape: Analysing petroleum product demand amid global geopolitical disruptions

30 June, 2026 16:23:51 IST

30 June, 2026 16:23:51 IST

DACL Fine Chem to set up Rs. 500-crore speciality chemicals facility at Kakinada SEZ

DACL Fine Chem Ltd, a Vadodara-based subsidiary of Diamines and Chemicals Ltd, is set to establish...

30 June, 2026 16:23:07 IST

Nuclear heat-based hydrogen facility commissioned at Kalpakkam

India has commissioned the world’s first hydrogen production facility based on the copper-chlorine thermochemical cycle using nuclear process...

30 June, 2026 16:22:06 IST

BPCL joins up with Shell and Tiki Tar to scale value-added bitumen business

Bharat Petroleum Corporation Ltd (BPCL) has signed a joint venture and share subscription agreement with Shell Gas B.V.,...

30 June, 2026 16:21:24 IST

MIT-WPU researchers develop solar thermal battery for post-sunset hot water

Researchers at Pune-based MIT World Peace University (MIT-WPU), a private university under the MIT Group of Institutions, have...

30 June, 2026 16:20:41 IST

Henkel appoints Pradhyumna Ingle as Country President for India

Henkel has appointed Mr. Pradhyumna Ingle as Country President for India, underscoring the company’s focus on one of...

30 June, 2026 16:19:47 IST

Fire at Haldia Petrochemicals’ naphtha pipeline injures around 20

A major fire broke out in a naphtha-carrying pipeline of Haldia Petrochemicals Ltd (HPL) in West...

30 June, 2026 16:19:15 IST

Aarav Fragrances & Flavors names Yatin Sheth as COO for ingredient business

Thane-based Aarav Fragrances & Flavors Pvt. Ltd., a manufacturer of fragrances, flavours, and specialty ingredients, has...

30 June, 2026 16:18:45 IST

OM Galaxy’s arm secures Indian patent for split-type hot runner manifold

Maharashtra-based OM Galaxy, a manufacturer of precision moulds for the plastic pipe fittings industry, has been...

30 June, 2026 16:18:05 IST

Zeon accelerates exit from ESBR and NBR latex business

Zeon Corporation is moving ahead with a major restructuring of its elastomers portfolio, accelerating its withdrawal...

30 June, 2026 16:17:27 IST

Kem One brings in new anchor shareholders to stabilise operations and cut debt

Kem One has reached an agreement in principle with its key financial partners on a sweeping...

30 June, 2026 16:16:56 IST

Restart of Ineos phenol plant in Antwerp postponed

Ineos Phenol has postponed the previously signalled late‑2027 restart of its Doel phenol plant in Antwerp,...

30 June, 2026 16:16:17 IST

Resonac to expand Japan’s HF gas capacity

Resonac will establish a two‑site production...

PRINT EDITION

Jun 30, 2026

View Digital Issue

Download Issue

View Past Issues

Search For

Exhibitions & Conferences

Watch

OTHER PUBLICATIONS

DATABASES