Latest Chemical Industry

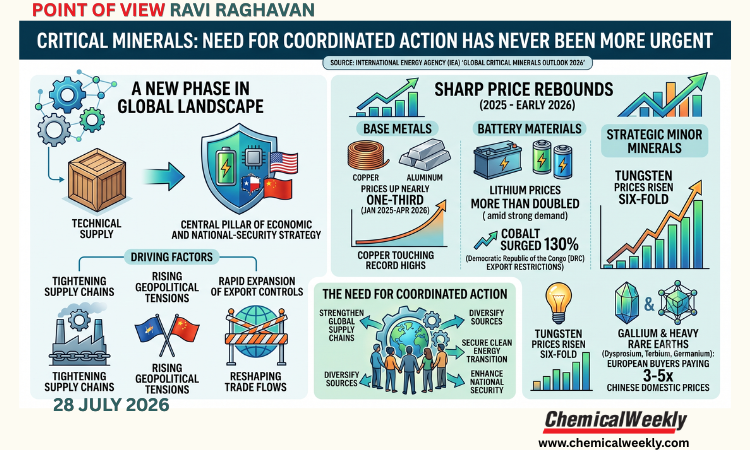

Critical minerals: Need for coordinated action has never been more urgent

28 July, 2026 17:28:50 IST

28 July, 2026 17:28:50 IST

Cabinet clears scheme for setting up three new chemical parks

The Union Cabinet has approved the Bhavya Rasayan Scheme (Bharat Audyogik Vikas Yojana Rasayan) with a...

28 July, 2026 17:27:16 IST

Epigral board approves Rs. 600‑crore epoxy resin & MPP expansion

The Board of Directors of Epigral Ltd. has approved a Rs. 600‑crore capex to enter the...

28 July, 2026 17:26:40 IST

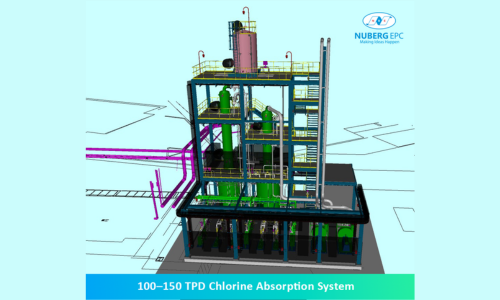

Nuberg EPC completes chlorine absorption system supply for Colombia's BRINSA

Noida-based Nuberg EPC has completed the design and supply of a 100-150-tpd Emergency Chlorine Absorption System...

28 July, 2026 17:26:04 IST

Atul board clears Rs. 167-crore downstream capex

Atul Ltd. has reported a sharp improvement in performance for Q1 FY27, with consolidated net profit...

28 July, 2026 17:25:35 IST

BTRA and MIDC partner to establish carbon fibre demonstration plant

The Bombay Textile Research Association (BTRA) and the Maharashtra Industrial Development Corporation (MIDC) have signed a...

28 July, 2026 17:24:53 IST

Aarti Drugs receives closure order for amines plant

Aarti Drugs Ltd. has received a 15‑day closure order from the Gujarat Pollution Control Board (GPCB)...

28 July, 2026 17:24:20 IST

Govt. imposes six‑month Minimum Import Price on suspension PVC

The government has restricted low‑priced imports of suspension‑grade PVC resin (S‑PVC) by imposing a minimum import...

28 July, 2026 17:23:43 IST

Air Products to supply gases to support semiconductor firm’s expansion in Taiwan

Air Products, the US-based industrial gases company, said its Taiwan arm, Air Products San Fu, has been awarded a...

28 July, 2026 17:23:06 IST

Kent bags detailed engineering contract for Oxea’s Texas project

Dubai-based Kent has been awarded detailed engineering services for a major specialty chemicals project at oxo...

28 July, 2026 17:22:34 IST

China’s Hunan Yuneng to invest $3.5-bn in integrated LFP mine-chemical project

Xiangtan-based Hunan Yuneng New Energy Battery Material Co., Ltd. has announced plans to invest approximately Yuan 24-bn ($3.5-bn)...

28 July, 2026 17:22:01 IST

Italy’s Versalis shuts polyethylene unit at Brindisi as Eni advances low-carbon transition

Italy-based Versalis, the chemicals subsidiary of Eni, has confirmed the shutdown of its polyethylene (PE) production unit at...

24 July, 2026 15:51:33 IST

CSIR-NCL hosts meet to advance Maharashtra’s green hydrogen ecosystem

The Center of Excellence (CoE) in Green Hydrogen Ecosystem Development at CSIR-National Chemical Laboratory (CSIR-NCL), Pune,...

PRINT EDITION

Jul 28, 2026

View Digital Issue

Download Issue

View Past Issues

Search For

Exhibitions & Conferences

Watch

OTHER PUBLICATIONS

DATABASES