Latest Chemical Industry

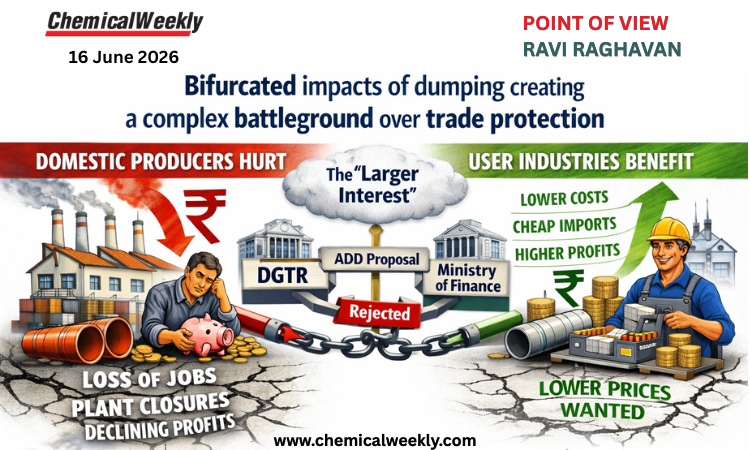

Bifurcated impacts of dumping creating a complex battleground over trade protection

19 June, 2026 15:06:26 IST

19 June, 2026 15:06:26 IST

AI startup Novyte Materials joins up with Chemvera Specialty Chemicals to bring novel polymer additive to market

Novyte Materials, a Mumbai-based AI-driven deep-tech startup, and Chemvera Specialty Chemicals, another Mumbai-based firm involved in speciality chemicals...

19 June, 2026 15:03:55 IST

N.A.N. GreenMet, Silox form battery recycling and critical minerals recovery jv

N.A.N. GreenMet, a Mumbai-based manufacturing platform founded by Mr. Navin Agarwal, Vice Chairman of Vedanta, and...

19 June, 2026 15:03:01 IST

Neuland readying new process development facility with integrated kilo labs in Hyderabad

Neuland Laboratories, Hyderabad-based contract development and manufacturing organisation (CDMO) specialising in complex APIs, is set to open a...

19 June, 2026 14:55:27 IST

Afton Chemical inks MoU with IOC

US-based manufacturer of fuel and lubricant additives Afton Chemical, has signed a Memorandum of Understanding with...

19 June, 2026 14:54:38 IST

SED gets Rs. 150-crore govt aid for ethanol biorefinery in UP

Mohali-based engineering company, Spray Engineering Devices Ltd (SED), has received approval for Rs....

19 June, 2026 14:53:31 IST

Osmo announces auction of exclusive licences for 10 AI-developed fragrance ingredients

US-based olfactory technology company, Osmo, has announced the “first-ever auction” of fragrance captive ingredients, offering exclusive...

19 June, 2026 14:52:35 IST

Evonik extends restructuring with 3,200 job cuts by 2029; to exit polyester business

German chemicals major Evonik Industries is significantly expanding its cost-reduction drive, announcing a further 3,200 job...

19 June, 2026 14:51:00 IST

Olin, Huntsman merge to create $12.5-bn chemicals group

US chemicals companies Olin Corporation and Huntsman Corporation have agreed to combine in an all-stock merger...

19 June, 2026 14:49:39 IST

Kemira acquires US-based Clear Water Technologies

Finland-based water treatment chemicals specialist, Kemira, has completed the acquisition of the business and related assets of Clear...

16 June, 2026 16:58:58 IST

Lubrizol, Grasim inaugurate CPVC resin plant in Gujarat

US-based chemicals major, Lubrizol, and Grasim Industries, a flagship company of the Aditya Birla Group, have...

16 June, 2026 16:57:45 IST

Srichakra ties up with Germany's Lindner Washtech for advanced PCR washing lines

Hyderabad-based producer of food-grade recycled plastics, Srichakra Polyplast, has entered into a technology partnership with Lindner...

16 June, 2026 16:56:40 IST

Sudarshan Chemical opens second global head office in Frankfurt

Pune-based pigment and colour solutions provider, Sudarshan Chemical Industries Ltd. has inaugurated its...

PRINT EDITION

Jun 23, 2026

View Digital Issue

Download Issue

View Past Issues

Search For

Exhibitions & Conferences

Watch

OTHER PUBLICATIONS

DATABASES