Page 189 - CW E-Magazine (8-4-2025)

P. 189

Special Report Special Report

India’s econ omic surge to drive global energy need to ensure energy security. But the 45% 30%

country will still need to import around

40%

demand, but with low-carbon twist 200-mt from seaborne markets. There- 35% 25%

fore, the current seaborne thermal coal

cost, approximately US$107 per tonne, 30% 20%

he country’s high-growth scena- The economy to reach just under and the adoption of electric vehicles could rise to US$110 per tonne by 2033. Increase fdrom base case 25% 15% India’s Share of global demand in high case

rio could triple India’s economy US$9-trillion, nearly triple from will further lower India’s energy inten- 20%

Tby 2033, but the impact on global US$3.2-trillion. sity. Emissions trajectory 15% 10%

energy markets differs from China’s Coal demand nearly doubles to 2.2- While CO emissions initially rise 10% 5%

2

boom billion tonnes. Modest impact on global energy due to the rapid expansion of coal, 5%

Oil demand to reach 8.2-million prices India’s high-growth scenario could 0% Coal Oil Gas Electricity Crude steel production 0%

India is set to become a major player barrels per day, up from 5.6-million In a high-growth scenario, while accelerate low-carbon supply chain Increase from base(LHS) Share of global demand in high case (RHS)

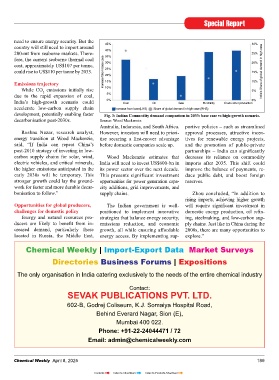

in the global energy markets with a barrels per day. competition for commodities is expected development, potentially enabling faster Fig. 3: Indian Commodity demand comparison in 2033: base case vs high-growth scenario.

unique growth path, featuring lower Power demand surges to almost to rise, India’s growing demand is not decarbonisation post-2030s. Source: Wood Mackenzie

energy intensity, a diverse energy mix 4,000 TWh, with signifi cant in- likely to trigger the signifi cant price Australia, Indonesia, and South Africa. portive policies – such as streamlined

and increased commodity imports, creases in both coal and renewable surges that occurred during China’s Roshna Nazar, research analyst, However, investors will need to priori- approval processes, attractive incen-

Wood Mackenzie’s latest Horizons generation. boom in the 2000s. The spare capacity energy transition at Wood Mackenzie, tise securing a fi rst-mover advantage tives for renewable energy projects,

report reveals. Steel demand to rise 9% annually, of OPEC+ is generally suffi cient to said, “If India can repeat China’s before domestic companies scale up. and the promotion of public-private

reaching 317-million tonnes accommodate the increasing oil demand post-2010 strategy of investing in low- partnerships – India can signifi cantly

The report, ‘Eye on the tiger: How from India. As a result, India’s oil demand carbon supply chains for solar, wind, Wood Mackenzie estimates that decrease its reliance on commodity

higher Indian economic growth could Different industrial structure is projected to increase Brent prices by electric vehicles, and critical minerals, India will need to invest US$600-bn in imports after 2035. This shift could

impact global energy markets’, high- India’s growth focuses on high- a relatively modest US$1 to US$3 per the higher emissions anticipated in the its power sector over the next decade. improve the balance of payments, re-

lights that, unlike China’s energy- value-added manufacturing, including barrel. early 2030s will be temporary. This This presents significant investment duce public debt, and boost foreign

intensive boom in the early 2000s, renewables and advanced batteries, stronger growth could lay the ground- opportunities for power generation capa- reserves.

India’s growth is expected to be more which is supported by government sub- The additional demand for 10-million work for faster and more durable decar- city additions, grid improvements, and

balanced, with a focus on high-value sidies and technological advancements. tons per annum (mtpa) of LNG bonisation to follow.” supply chains. Zhou concluded, “In addition to

manufacturing and renewable energy. from India will arise during a period rising imports, achieving higher growth

Lower energy intensity when global gas prices are expected Opportunities for global producers, The Indian government is well- will require signifi cant investment in

“India’s growth story shares simi- India’s industrial sector currently to decline. The market is preparing to challenges for domestic policy positioned to implement innovative domestic energy production, oil refi n-

larities with China’s rapid expansion, consumes less energy per unit of GDP absorb more than 200-mtpa of LNG Energy and natural resources pro- strategies that balance energy security, ing, steelmaking, and low-carbon sup-

but crucial differences set it apart,” said than China did in the early 2000s. By supply growth, which accounts for ducers are likely to benefi t from in- emissions reduction, and economic ply chains. Just like in China during the

Yanting Zhou, Principal Economist 2033, crude steel and cement produc- about 50% of current supply, limiting creased demand, particularly those growth, all while ensuring affordable 2000s, there are many opportunities to

at Wood Mackenzie. “While energy tion in India is projected to be only potential price increases for LNG. located in Russia, the Middle East, energy access. By implementing sup- explore.”

demand will surge, India’s industrial about one-third of China’s output in

sector is less energy-intensive, and the 2011, according to Wood Mackenzie’s India’s thermal coal production Chemical Weekly | Import-Export Data Market Surveys

country is better positioned to adopt high-growth scenario. Additionally, an could reach 1,800-mt by 2033 in the

efficient, low-carbon technologies increasing share of renewable energy high-growth scenario, driven by the Directories Business Forums | Expositions

compared to China in the 2000s.”

The only organisation in India catering exclusively to the needs of the entire chemical industry

This unique trajectory could accele-

rate India’s transition to a low-carbon

economy, potentially enabling the Contact:

nation to achieve its net-zero emissions SEVAK PUBLICATIONS PVT. LTD.

goal ahead of the 2070 target. 602-B, Godrej Coliseum, K.J. Somaiya Hospital Road,

According to Wood Mackenzie’s Behind Everard Nagar, Sion (E),

high-growth scenario for India (in Mumbai 400 022.

which the Indian economy between India India 2023 India 2033 China India India 2033 India 2033 China

high case 2011

2023

base case

2011

2023

base case high case

2024 and 2033 achieves a similar level GDP (LHS) GDP per capita (RHS) Total energy consumption (LHS) Energy intensity (RHS) Phone: +91-22-24044471 / 72

of growth to the Chinese economy Fig. 1: India vs China GDP Comparison. Fig. 2: India vs China Energy Demand Email: admin@chemicalweekly.com

between 2001 and 2011), by 2033: Source: Wood Mackenzie Comparison

188 Chemical Weekly April 8, 2025 Chemical Weekly April 8, 2025 189

Contents Index to Advertisers Index to Products Advertised