Page 192 - CW E-Magazine (19-11-2024)

P. 192

Special Report

rates by ~250 bps but remained com-

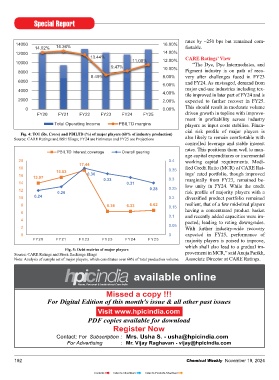

14000 16.00%

14.02% 14.36% fortable.

12000 14.00%

13.44% CARE Ratings’ View

10000 11.00% 12.00% “The Dye, Dye Intermediates, and

9.47% 10.00%

8000 Pigment industry is on path of reco-

8.49% 8.00% very after challenges faced in FY23

6000 and FY24. As envisaged, demand from

6.00%

4000 major end-use industries including tex-

4.00% tile improved in later part of FY24 and is

2000 2.00% expected to further recover in FY25.

0 0.00% This should result in moderate volume

FY20 FY21 FY22 FY23 FY24 FY25 driven growth in topline with improve-

ment in profi tability across industry

Total Operating Income PBILTD margins players as input costs stabilise. Finan-

cial risk profi le of major players is

Fig. 4: TOI (Rs. Crore) and PBILTD (%) of major players (60% of industry production)

Source: CARE Ratings and BSE fi lings; FY24 are Estimates and FY25 are Projections also likely to remain comfortable with

controlled leverage and stable interest

rates. This positions them well to man-

PBILTD Interest coverage Overall gearing

age capital expenditures or incremental

20 0.4 working capital requirements. Modi-

17.44

18 0.35 fi ed Credit Ratio (MCR) of CARE Rat-

15.53

16 13.97 0.36 ings’ rated portfolio, though improved

14 0.33 0.31 0.3 marginally from FY23, remained be-

low unity in FY24. While the credit

12 0.26 0.28 0.25 risk profi le of majority players with a

10 0.24 0.2 diversifi ed product portfolio remained

8 6.36 6.33 6.62 0.15 resilient, that of a few mid-sized players

6 having a concentrated product basket

0.1 and recently added capacities were im-

4 pacted; leading to rating downgrades.

2 0.05 With further industry-wide recovery

0 0 expected in FY25, performance of

FY20 F Y21 FY22 FY23 FY24 F Y25 majority players is poised to improve,

Fig. 5: Debt metrics of major players which shall also lead to a gradual im-

Source: CARE Ratings and Stock Exchange fi lings provement in MCR,” said Anuja Parikh,

Note: Analysis of sample set of major players, which constitutes over 60% of total production volume. Associate Director at CARE Ratings.

Mrs. Usha S. - usha@hpicindia.com

192 Chemical Weekly November 19, 2024

Contents Index to Advertisers Index to Products Advertised