Page 185 - CW E-Magazine (6-8-2024)

P. 185

Special Report Special Report

stocks. Light naphtha produced in the steam cracker operating companies or

refi nery as a feedstock for steam crack- traders serving the chemical industry.

ing and reformate for aromatics as well The output PyOil is typically fraction-

as fuels production can thus have an ated and while some co-processing in

attributed renewable content. Renew- refi neries can take place, an upgrading

able feedstocks may be attributed to fuels of the PyOil (typically via hydrotreat-

or chemicals or proportions of each. ment) to remove contaminants is essen-

tial where it is to be processed by steam

HVO/HEFA crackers.

The process known as hydrotreated

or hydrogenated vegetable oil (HVO) The number of plastics pyrolysis

or hydrogenated esters and fatty acids plants linked to downstream partners

(HEFA), is one which has been deve- or offtakers is relatively small as of

loped primarily to produce bio-based 2023, with Europe leading as a region

diesel and/or SAF (synthetic aviation in the number of plants – estimated at

fuel) via hydrogenation (hydrotreat- 18 currently. The number of projects is

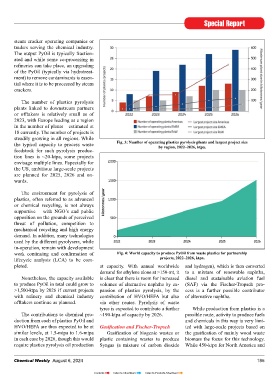

ment) and hydrocracking of bio-based Fig. 2: World production of renewable (bio-based) steam cracker feedstock steadily growing in all regions. While

feedstocks which include vegetable from HVO/HEFA, 2022–2026, kt. the typical capacity to process waste Fig. 3: Number of operating plastics pyrolysis plants and largest project size

by region, 2022–2026, ktpa.

oils, waste oils such as used cooking oil wide in 2023, the number of companies Unlike HVO/HEFA outputs, PyOil feedstock for such pyrolysis produc-

and by-products from the processing of active in providing feedstock for attri- is not a by-product of fuels produc- tion lines is ~20-ktpa, some projects

palm oil as well as tall oil, a by-product buted chemicals via steam cracking is tion. The PyOil in total or fractions of envisage multiple lines. Especially for

of the wood pulp and paper industry. very much smaller and dominated by the PyOil could also be used as fuel, the US, ambitious large-scale projects

four key companies. though when used in this way, circula- are planned for 2025, 2026 and on-

Production via HVO/HEFA has rity is lost. wards.

been taking place since the early/mid In 2023, approximately 1.15-mt in

2010’s and overall output volumes have total of renewable naphtha (RN) and Proposed new EU legislation now The environment for pyrolysis of

increased sharply since 2000. World renewable diesel (RD) were estimated sets ambitious targets for recycled plastics, often referred to as advanced

capacity in 2023 was estimated at 18.2- to be used as steam cracker feedstock content in plastic packaging materials. or chemical recycling, is not always

mtpa worldwide with planned projects from which renewable attributed pro- Pyrolysis as a form of recycle offers supportive – with NGO’s and public

to take capacity to close to 40-mtpa by ducts were made. Based on currently great advantages in achieving the qua- opposition on the grounds of perceived

2026. As well as bio-based diesel and known projects, production for the lity standards that packaging materials threat of pollution, competition to

SAF, one output of the process is bio- chemical industry is expected to rise to in contact sensitive applications must mechanical recycling and high energy

based naphtha at levels up to ~10% approximately 1.6-mt by 2026. achieve. Legislation has not offi cially demand. In addition, many technologies

of total output. been introduced into EU law yet, but used by the different pyrolysers, while

Pyrolysis Oil (PyOil) from waste plas- it can be expected that pyrolysis and in-operation, remain with development

Bio-based naphtha, and dependent tics and tyres other chemical recycling technologies work continuing and confi rmation of Fig. 4: World capacity to produce PyOil from waste plastics for partnership

on the confi guration of the steam cracker, Pyrolysis oil from the treatment of will thus play a signifi cant role in lifecycle analysis (LCA) to be com- projects, 2022–2026, ktpa.

renewable (bio-based) diesel from waste plastics or end of life tyres, via achieving more ambitious recycling pleted. at capacity. With annual worldwide and hydrogen), which is then converted

the HVO/HEFA process can replace “chemical recycling” or of biomass is targets and strongly support the produc- demand for ethylene alone at >150-mt, it to a mixture of renewable naphtha,

fossil based light naphtha as a steam a second source of “alternative naphtha” tion of PyOil from plastic wastes. Nonetheless, the capacity available is clear that there is room for increased diesel and sustainable aviation fuel

cracker feedstock. (Steam cracking for the chemical industry. The pyrolysis to produce PyOil in total could grow to volumes of alternative naphtha by ex- (SAF) via the Fischer-Tropsch pro-

operations vary considerably worldwide of plastics and tyres has grown signi- Tyre-derived PyOil contains a signifi - >1,500-ktpa by 2026 if current projects pansion of plastics pyrolysis, by the cess is a further possible contributor

regarding acceptance of feedstocks. fi cantly in interest in the past 2-3 years cant bio-based content from the natural with refi nery and chemical industry contribution of HVO/HEFA but also of alternative naphtha.

In the US and Middle East, steam because it is not only a means of rubber used in tyre manufacture, making offtakers continue as planned. via other routes. Pyrolysis of waste

crackers are set-up for lighter ethylene treatment of plastic containing wastes it attractive, in the case where a bio-based tyres is expected to contribute a further While production from plastics is a

or gas-based feedstocks and not neces- which are often diffi cult to recycle by share receives incentives. The contributions to chemical pro- ~190-ktpa of capacity by 2026. possible route, activity to produce fuels

sarily suitable for processing bio-based mechanical means, but also because it duction from each of plastics PyOil and and chemicals in this way is very limi-

naphtha). offers the potential for a level of circu- The industry is characterised by HVO/HEFA are thus expected to be at Gasifi cation and Fischer-Tropsch ted with large-scale projects based on

larity for plastics able to complement partnerships between developers and similar levels, at 1.5-mtpa to 1.6-mtpa Gasifi cation of biogenic wastes or the gasifi cation of mainly wood waste

While there were an estimated 44 other sources of renewable feedstock operators of pyrolysis technologies and in each case by 2026, though this would plastic containing wastes to produce biomass the focus for this technology.

HVO/HEFA producing facilities world- for refi neries and steam cracking. downstream partners – the refi nery and require plastics pyrolysis oil production Syngas (a mixture of carbon dioxide While 450-ktpa for North America and

184 Chemical Weekly August 6, 2024 Chemical Weekly August 6, 2024 185

Contents Index to Advertisers Index to Products Advertised