Page 133 - CW E-Magazine (6-8-2024)

P. 133

Point of View

LNG imports will make up for slack in domestic natural

gas output

Natural gas is widely seen as a transition fuel in

the journey to more sustainable energy, especially

for countries reliant on coal to meet a large portion

of their energy. This includes India, and planners

here have been aiming to have gas play a much

larger role than now. But India is constrained with

poor natural gas resources and reserves, and

despite some recent successes in the Krishna-

Godavari (KG) basin, supply is far below what the

markets need.

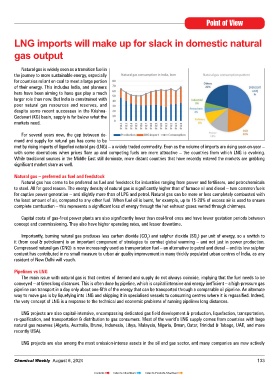

For several years now, the gap between de-

mand and supply for natural gas has come to be

met by rising imports of liquefied natural gas (LNG) – a widely traded commodity. Even as the volume of imports are rising year-on-year –

with some aberrations when prices flare up and competing fuels are more attractive – the countries from which LNG is evolving.

While traditional sources in the Middle East still dominate, more distant countries that have recently entered the markets are grabbing

significant market share as well.

Natural gas – preferred as fuel and feedstock

Natural gas has come to be preferred as fuel and feedstock for industries ranging from power and fertilisers, and petrochemicals

to steel. All for good reason. The energy density of natural gas is significantly higher than of furnace oil and diesel – two common fuels

for captive power generation – and slightly more than of LPG and petrol. Natural gas can be more or less completely combusted with

the least amount of air, compared to any other fuel. When fuel oil is burnt, for example, up to 15-20% of excess air is used to ensure

complete combustion – this represents a significant loss of energy through the hot exhaust gases vented through chimneys.

Capital costs of gas-fired power plants are also significantly lower than coal-fired ones and have lower gestation periods between

concept and commissioning. They also have higher operating rates, and lesser downtime.

Importantly, burning natural gas produces less carbon dioxide (CO ) and sulphur dioxide (SO ) per unit of energy, so a switch to

2

2

it (from coal & petroleum) is an important component of strategies to combat global warming – and not just in power production.

Compressed natural gas (CNG) is now increasingly used as transportation fuel – an alternative to petrol and diesel – and its low sulphur

content has contributed in no small measure to urban air quality improvement in many thickly populated urban centres of India, as any

resident of New Delhi will vouch.

Pipelines vs LNG

The main issue with natural gas is that centres of demand and supply do not always coincide, implying that the fuel needs to be

conveyed – at times long distances. This is often done by pipeline, which is capital intensive and energy inefficient – a high-pressure gas

pipeline can transport in a day only about one-fifth of the energy that can be transported through a comparable oil pipeline. An alternate

way to move gas is by liquefying into LNG and shipping it in specialised vessels to consuming centres where it is regassified. Indeed,

the very concept of LNG is a response to the technical and economic problems of running pipelines long distances.

LNG projects are also capital-intensive, encompassing dedicated gas field development & production, liquefaction, transportation,

re-gasification, and transportation & distribution to gas consumers. Most of the world’s LNG supply comes from countries with large

natural gas reserves (Algeria, Australia, Brunei, Indonesia, Libya, Malaysia, Nigeria, Oman, Qatar, Trinidad & Tobago, UAE, and more

recently USA).

LNG projects are also among the most emission-intense assets in the oil and gas sector, and many companies are now actively

Chemical Weekly August 6, 2024 133

Contents Index to Advertisers Index to Products Advertised